Demos

Demos  Colors

Colors

Docs

Docs  Support

Support

No products in the cart.

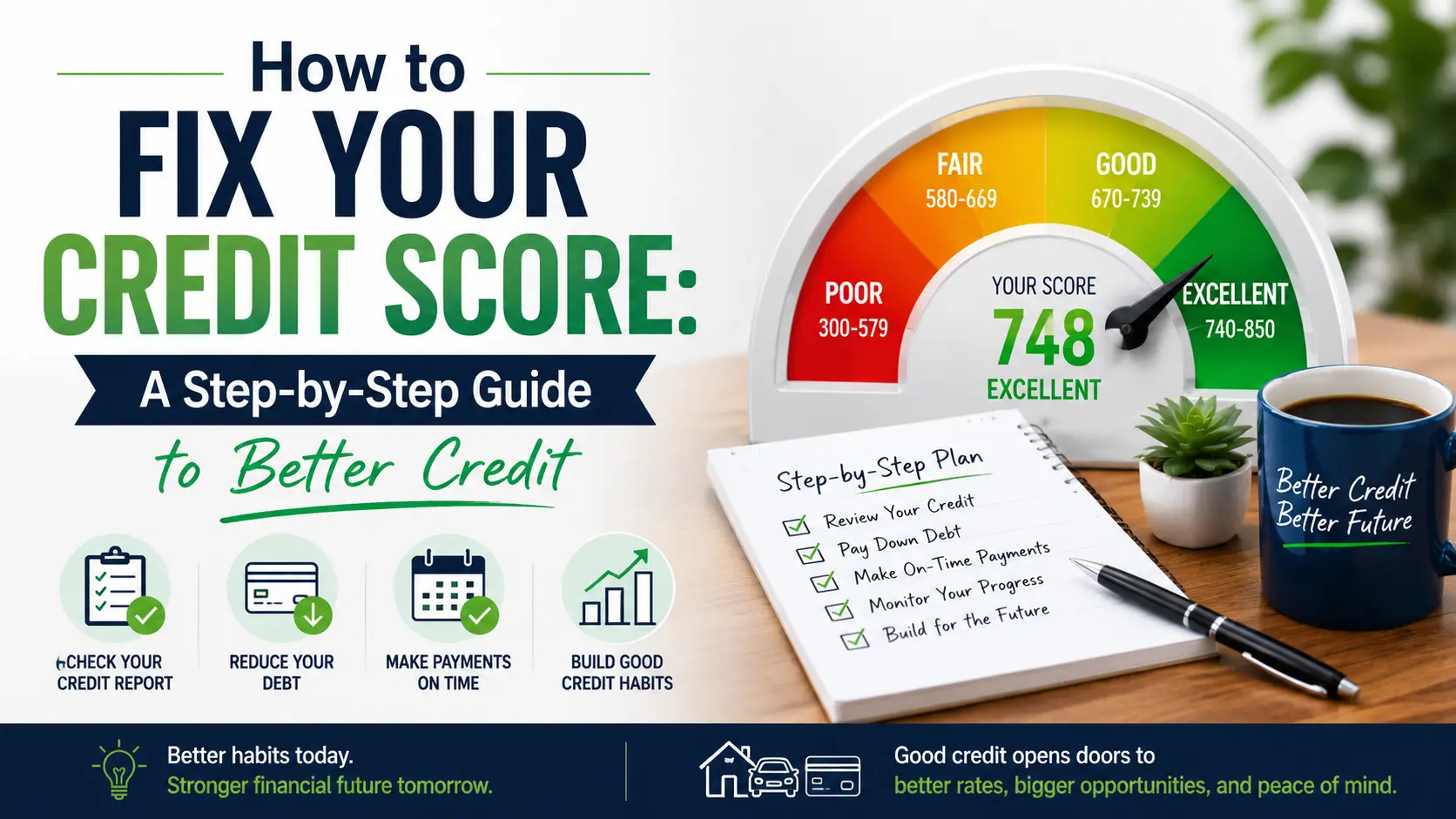

Practical, proven strategies to understand, repair, and rebuild your credit — starting today.

Your credit score is one of the most powerful numbers in your financial life. It shapes whether you get approved for a mortgage, what interest rate you’ll pay on a car loan, and sometimes even whether you land that job you want. The good news? No matter where your score stands right now, you can improve it — and this guide will show you exactly how.

Millions of Americans are living with damaged or limited credit, and most of them feel stuck. But credit repair is not a mystery. It’s a process. It takes patience, consistency, and knowing which actions actually move the needle. Let’s walk through it together.

STEP ONE

Pull Your Credit Reports and Know What You’re Dealing With

You cannot fix what you haven’t seen. The very first thing to do is get a copy of your credit reports from all three major bureaus — Equifax, Experian, and TransUnion. You’re entitled to a free report from each bureau once a year through AnnualCreditReport.com, the only federally authorized source.

Read each report carefully. Look for accounts you don’t recognize, late payments that seem wrong, balances that appear incorrect, and anything that seems out of place. Note every negative item along with its date — this matters, because most negative marks fall off your report after seven years.

Pro Tip: Stagger Your Reports Instead of pulling all three reports at once, consider requesting one every four months. That way, you’re monitoring your credit for free throughout the entire year.

Step Two

Dispute Errors — They’re More Common Than You Think

Studies have found that roughly one in five Americans has at least one error on their credit report. These mistakes can drag down your score significantly, and the best part is they’re fixable — often within 30 to 45 days.

If you spot something inaccurate, you have the legal right under the Fair Credit Reporting Act (FCRA) to dispute it. You can file disputes directly with each credit bureau online, by mail, or by phone. When disputing, be specific: include your name, the account in question, why you believe it’s an error, and any supporting documentation (bank statements, letters from creditors, etc.).

- Accounts that don’t belong to you (possible identity theft or mixed files)

- Incorrect payment statuses — e.g., a payment marked “late” that you made on time

- Outdated negative items that should have aged off your report

- Duplicate accounts appearing more than once

- Wrong balances or credit limits

- Closed accounts incorrectly listed as open (or vice versa)

After filing a dispute, the bureau is required to investigate — typically within 30 days — and inform you of the result. If the error is corrected, your score can improve almost immediately.

Step Three

Understand What Actually Makes Up Your Score

Before you can improve your score, you need to understand how it’s calculated. The most widely used model, FICO, breaks your score into five weighted categories:

| Factor | Weight | What It Means |

| Payment History | 35% | Whether you pay your bills on time — the single biggest factor. |

| Credit Utilization | 30% | How much of your available revolving credit you’re using. |

| Length of Credit History | 15% | How long your accounts have been open, on average. |

| Credit Mix | 10% | Variety of credit types: cards, loans, mortgage, etc. |

| New Credit | 10% | Recent applications for credit (hard inquiries). |

Knowing these weights tells you where to put your energy. Paying on time and reducing your balances alone address 65% of your score.

Step Four

Pay Every Bill On Time — Without Exception

Payment history is the heavyweight champion of credit scoring. One missed payment can drop your score by 50 to 100 points or more, and that damage can linger on your report for seven years. On the flip side, a consistent track record of on-time payments is the most reliable way to build your score back up over time.

The practical fix here is simple: set up autopay for at least the minimum payment on every account. Not everyone loves autopay — and that’s okay — but if you have a history of forgetting due dates, it’s a safety net worth using. Calendar reminders, budgeting apps, and bank alerts are also great tools for staying on top of payments.

“Consistency is the foundation of credit repair. One good month won’t transform your score — but twelve good months will.”

— Permissible LLC Financial Guidance Team

If you have past-due accounts, bring them current as quickly as possible. The longer an account stays delinquent, the more it damages your score — and once you bring it current, the positive reporting begins immediately.

Step Five

Lower Your Credit Utilization Ratio

Credit utilization is the percentage of your available revolving credit that you’re currently using. If your credit card limit is $5,000 and your balance is $2,500, your utilization is 50% — and that’s considered high. Most experts recommend keeping utilization below 30%, and for those aiming for excellent credit, below 10%.

Here’s what makes this factor particularly powerful: it can improve quickly. Unlike late payments that take years to fade, reducing your balances can boost your score within a single billing cycle. Some strategies to lower utilization include:

- Pay down high-balance cards first, especially those close to their limit

- Make multiple smaller payments throughout the month rather than one at the end

- Request a credit limit increase on existing cards (without increasing spending)

- Avoid closing old credit card accounts — this reduces your total available credit

- Spread balances across multiple cards rather than maxing out one

Step Six

Build (or Rebuild) Credit Strategically

If your credit history is thin or severely damaged, you may need to start fresh — and there are safe, effective ways to do that. A few options worth considering:

Secured credit cards are among the most accessible tools for rebuilding credit. You put down a deposit (typically $200–$500) that becomes your credit limit. Use it for small purchases and pay the balance in full each month. After 12 to 18 months of responsible use, many issuers will upgrade you to a regular unsecured card and return your deposit.

Credit-builder loans are offered by many credit unions and community banks. You make monthly payments into a savings account, and the lender reports those payments to the bureaus. When the loan term ends, you get the money. It’s structured savings that builds credit at the same time.

Becoming an authorized user on a family member’s or trusted friend’s credit card can give your score a boost — as long as the primary cardholder has a solid payment history and low utilization. Their good behavior gets reported on your credit profile too.

Watch Out for Credit Repair Scams

Be cautious of companies promising to “erase” bad credit overnight or guaranteeing a specific score increase. Legitimate credit repair takes time. No one can legally remove accurate negative information from your report before its time. If it sounds too good to be true, it almost certainly is.

Step Seven

Be Strategic About New Credit Applications

Every time you apply for new credit, the lender typically performs a “hard inquiry” on your report, which can temporarily lower your score by a few points. This isn’t usually a big deal for a single inquiry, but applying for multiple credit products in a short period can signal financial desperation to lenders and accumulate quickly.

A few ground rules: only apply for credit you genuinely need, space out your applications, and when rate shopping for a mortgage, car loan, or student loan, try to do all your inquiries within a 14–45 day window (depending on the scoring model). Multiple inquiries for the same loan type during this period are typically treated as a single inquiry.

Step Eight

Protect What You’ve Built

As your score climbs, your focus shifts from repair to maintenance. That means continuing the habits that got you here: paying on time, keeping balances low, and only applying for credit when necessary. It also means staying vigilant about identity theft — one of the fastest ways to derail credit progress.

Consider placing a free credit freeze with all three bureaus if you’re not actively applying for credit. A freeze prevents new accounts from being opened in your name without your knowledge. You can lift and refreeze it at any time. Also sign up for credit monitoring — many banks and credit card issuers offer this for free now — so you get notified the moment anything changes on your report.

- Set up free credit monitoring through your bank or a service like Credit Karma

- Review your full credit reports at least once a year

- Keep old accounts open even if you don’t use them (they help your length of history)

- Stay below 30% utilization as a long-term habit, not just a one-time fix

- Respond immediately if you see unfamiliar activity on any report

Final Thoughts

Better Credit Is a Journey, Not a Quick Fix

Rebuilding credit doesn’t happen in a week, and that’s actually okay. What you’re building isn’t just a number — it’s a track record of financial trustworthiness that opens real doors: lower interest rates, better loan terms, more housing options, and more financial freedom overall.

Start with what you can control right now: pull your reports, dispute errors, pay on time, and chip away at balances. Each step compounds on the last. Six months from now, you’ll look back and be surprised how far you’ve come.

At Permissible LLC, we believe everyone deserves access to clear, honest financial information. If you have questions about your credit situation or want personalized guidance, don’t hesitate to reach out to our team.